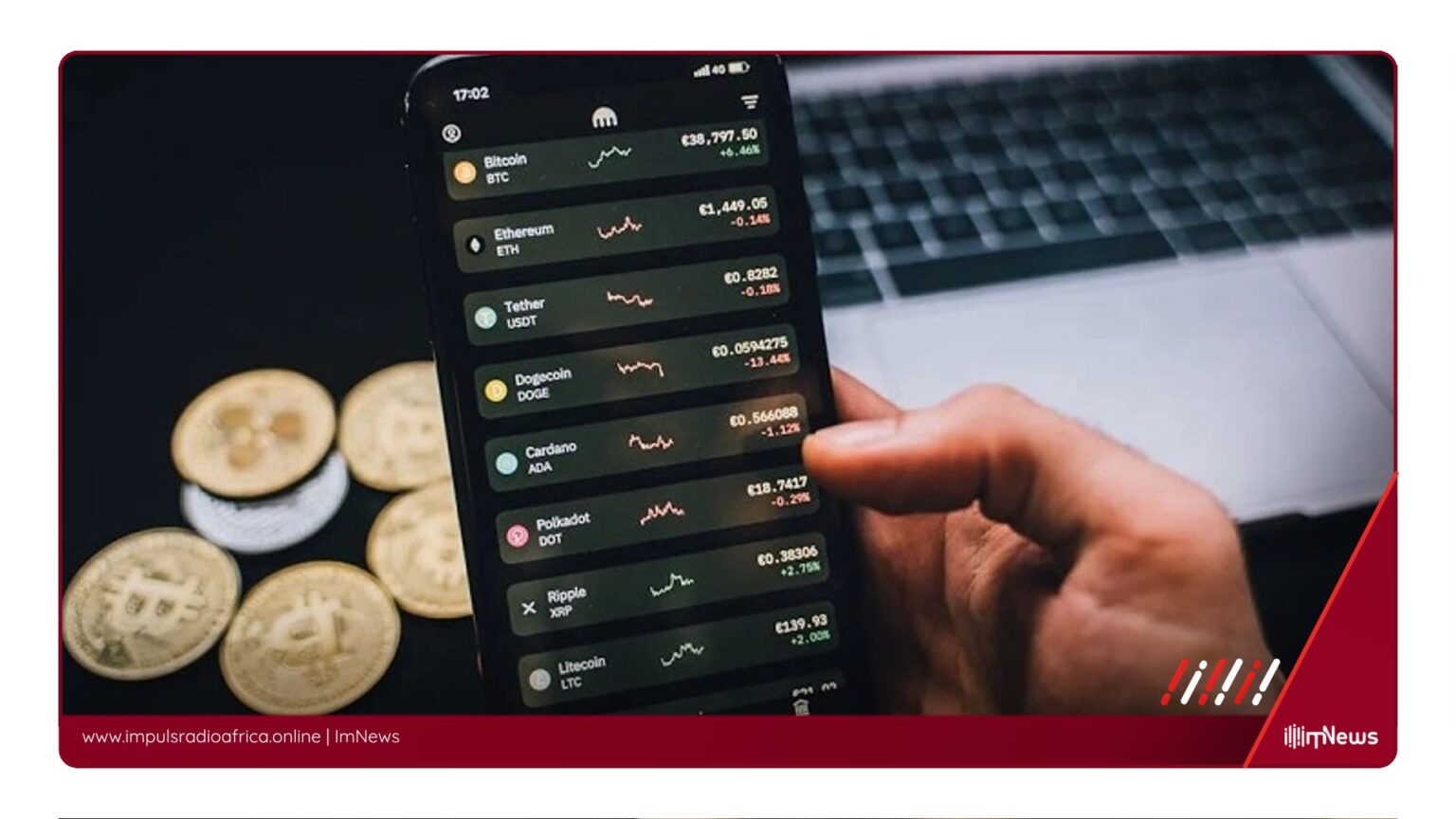

Nairobi, Kenya — In a landmark move, Kenya is set to introduce a new law that mandates virtual asset service providers to submit annual reports to the Kenya Revenue Authority (KRA), detailing customer activities, including transaction histories and wallet information. This initiative, outlined in the Finance Bill 2026, represents a significant step towards greater transparency and tax compliance within the country’s burgeoning cryptocurrency market.

The Bill, currently under consideration by the Kenyan Parliament, proposes that crypto platforms operating in Kenya identify customers and disclose information linked to reportable users and controlling persons. It reflects a global trend of governments intensifying efforts to monitor digital asset transactions, improve tax collection, and curb money laundering through cryptocurrencies. Kenya’s push for stricter regulations comes as the country’s cryptocurrency market has experienced a surge, with transactions totaling an estimated KES 2.

4 trillion ($18. 5 billion) between 2021 and 2022.

The new rules aim to provide tax authorities with direct visibility into the trading activities of digital assets, how much they are earning, and where funds are moving.

The Finance Bill 2026 also includes provisions that would allow the KRA to exchange crypto-related tax information with foreign governments under international reporting agreements. This aligns with the Organisation for Economic Co-operation and Development’s Cryptoasset Reporting Framework (CARF), which took effect in January 2026 and requires participating countries to collect and exchange data on crypto transactions across borders. Supporters of the new measures argue that they will enhance transparency and cooperation between Kenyan authorities and foreign governments in combating illicit crypto transactions and tax evasion.

Critics, however, caution that the strict reporting requirements may impose additional compliance burdens on exchanges and potentially discourage users from engaging in cryptocurrency trading.

The proposals within the Finance Bill 2026 reflect the growing importance of digital assets in Kenya’s economy. If passed, the Bill would allow Kenya to exchange crypto-related tax information with foreign governments under international agreements, further solidifying the country’s position as a leader in crypto regulation on the continent.

The introduction of the new crypto disclosure law in Kenya represents a significant development in the regulation of the digital asset market.

As Africa’s crypto sector continues to grow, the need for robust regulatory frameworks to ensure transparency and compliance with tax laws becomes increasingly apparent. Kenya’s approach may serve as a model for other African countries looking to harness the potential of digital assets while mitigating associated risks.

*Additional reporting by ImNews | Sources consulted: 5*

—

This original article was produced by the ImNews editorial team

Source: Africa.businessinsider

Source: Ayodeji Adegboyega